Small and medium size businesses often struggle to access to credit from traditional lenders like banks. Finding suitable alternatives to help businesses obtain credit can solve larger problems of economic development in many developing countries; Nigeria’s successful experiment has demonstrated that access to small business funding is a major impediment to growth.

Banks may be reluctant to provide loans to small businesses, but they are no longer the sole credit providers. A new report produced by Tradeup looks at how SMEs funding has changed since the financial crisis of 2008. A number of alternative investment models have emerged or expanded in response to the 2008 financial crisis, research found.

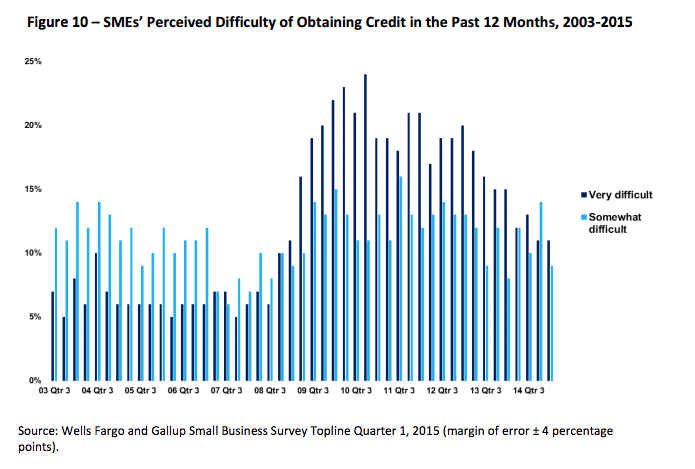

The graph below shows small businesses’ perceived difficulty of obtaining credit. As expected, the chart signals a turning point after the financial crisis, when banks seemed increasingly reluctant to provide credit to small businesses. Since 2008, however, SME financing has changed considerably: when traditional sources of credit failed to meet the demand of SMEs, new forms of lending began to develop. The report takes a closer look at three main types of nonbank lending practices.

1. Online Nonbank Lenders

The use of online lending platforms has increased dramatically since 2008. In 2014, over $8.6 billion in loans were awarded through online nonbank lenders. Online lenders used proprietary analytics to determine the borrowers’ worthiness. While banks look at typical metrics such as cash flow and profitability, these lenders tend to factor in alternative metrics including business owners’ credit card records and social media feed back.

There are three main types of online lending structures: balance sheets, marketplaces, and those that connect prime quality borrowers to capital. The rates and terms vary considerably: online balance sheets, which use balance sheet capital to make decisions, like OnDeck and Kabbage tend to have higher APRs and shorter terms than P2P platforms like the Lending Club or Funding Circle, which connect prime and superprime quality borrowers with quality capital from consumers and international investors.

In December 2014, two of the largest online lending platforms, Lending Club and Dealstruck had IPOs, for a total of $6.7 billion.

2. Crowdfunding

Crowdfunding helps companies raise donations, debt or equity from individuals and institutions, typically for less than $250,000. Between 2010 and 2014, the crowdfunding market grew from $1 billion valued at $10 billion.

In recent years, crowdfunding has shifted from a platform to support artistic, philanthropic and social endeavors into a format for entrepreneurs to support their projects. At the time the study was completed, there were more than 350 crowdfunding platforms in the US and more than 80 in the UK.

3. Angel Investing and Venture Capital

Angel investing and venture capital investments may not be novel, but they have become an important alternative to bank lending since 2008. In 2014, there was a total of 4,356 venture capital investments deals for a combined $48.3 billion, then highest since the dot com boom of 2000. While the majority of deals were for early-stage companies, expansion-stage deals received the most investment capital.

Angel investments are made by individual investors who directly lend to companies. As the size of venture capital investments have increased for expansion-stage firms, angels filled the gap for smaller, promising firms.

Looking Forward

As alternative methods for obtaining credit become more accepted, more small and medium enterprises are able to grow, a promising trend in light of the strong links between high growth firms and job creation.

To read the full report on SME finance in the United States, please click here.

No Comments